Chapter 24 Tidymodels vs Scikit-learn

Scikit-learn, like tidymodels, is a framework to define machine learning models and train them.

As an open-source project, it has a large community of contributors and users. It is well-documented and has a wide range of algorithms and tools for data preprocessing, model selection, and evaluation. It is the de facto standard for machine learning in Python.

Even if models have no direct implementation in scikit-learn, the third-party libraries often implement the scikit-learn API, making them compatible with the framework. xgboost is a popular example for this.

There are many parallels between Tidymodels and scikit-learn; both have a similar approach to model definition and training. You will recognize many of the ideas and concepts from the tidymodels framework in scikit-learn.

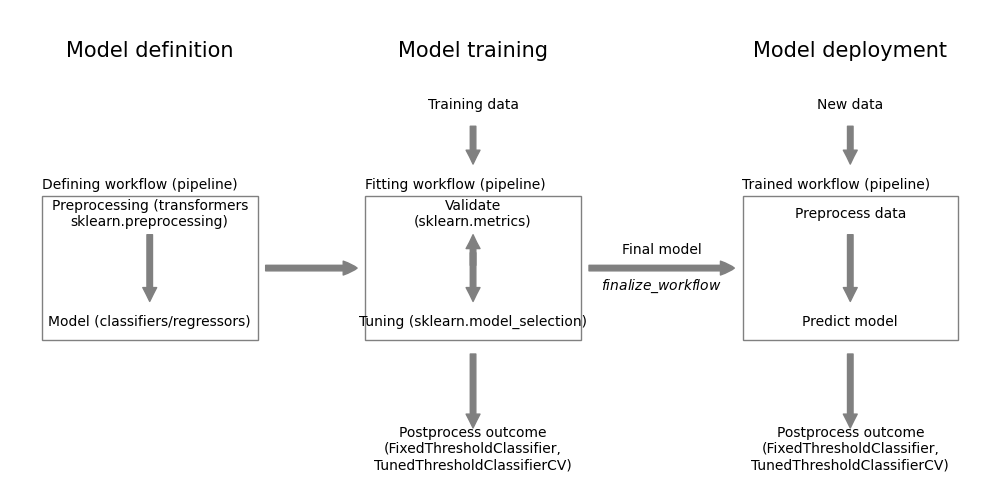

Figure 24.1 shows the Python packages mapped onto the modeling workflow of Figure 6.1.

Figure 24.1: Modeling workflow

24.1 Load required packages

Like in R, we start with the import of the required packages:

Code

Python:

Code

import pandas as pd

import matplotlib.pyplot as plt

from sklearn import preprocessing

from sklearn.model_selection import (train_test_split, RandomizedSearchCV,

cross_val_predict)

from sklearn.compose import ColumnTransformer

from sklearn.pipeline import Pipeline

from sklearn.linear_model import LogisticRegressionR:

24.2 Load the data

Code

data <- read_csv("https://gedeck.github.io/DS-6030/datasets/loan_prediction.csv",

show_col_types=FALSE) %>%

drop_na() %>%

mutate(

Gender=as.factor(Gender),

Married=as.factor(Married),

Dependents=gsub("\\+", "", Dependents) %>% as.numeric(),

Education=as.factor(Education),

Self_Employed=as.factor(Self_Employed),

Credit_History=as.factor(Credit_History),

Property_Area=as.factor(Property_Area),

Loan_Status=factor(Loan_Status, levels=c("N", "Y"), labels=c("No", "Yes"))

) %>%

select(-Loan_ID)Code

data = pd.read_csv("https://gedeck.github.io/DS-6030/datasets/loan_prediction.csv")

data = data.dropna()

data['Dependents'] = [int(str(s).strip('+')) for s in data['Dependents']]

data['Loan_Status'] = [1 if s == 'Y' else 0 for s in data['Loan_Status']]

outcome = 'Loan_Status'

predictors = ['Gender', 'Married', 'Dependents', 'Education', 'Self_Employed',

'ApplicantIncome', 'CoapplicantIncome', 'LoanAmount', 'Loan_Amount_Term',

'Credit_History', 'Property_Area']24.3 Split the data into training and holdout data

Split dataset into training and holdout data

Code

Code

## ((384, 11), (96, 11), (384,), (96,))24.4 Define the model

R:

Code

formula <- Loan_Status ~ Gender + Married + Dependents + Education + Self_Employed +

ApplicantIncome + CoapplicantIncome + LoanAmount + Loan_Amount_Term +

Credit_History + Property_Area

recipe_spec <- recipe(formula, data=train_data) %>%

step_dummy(all_nominal(), -all_outcomes())

# recipe_spec %>% prep() %>% bake(new_data=NULL) %>% head()

model_spec <- logistic_reg(engine="glmnet", mode="classification",

penalty=tune(), mixture=0)

wf <- workflow() %>%

add_model(model_spec) %>%

add_recipe(recipe_spec)Python:

Code

preprocess = ColumnTransformer([

('encoder', preprocessing.OneHotEncoder(drop='first'),

['Gender', 'Married', 'Education', 'Self_Employed', 'Property_Area']),

('unchanged', 'passthrough',

['Dependents', 'ApplicantIncome', 'CoapplicantIncome', 'LoanAmount',

'Loan_Amount_Term', 'Credit_History']),

])

# preprocess.fit_transform(data).round(4)[:20,]

model = Pipeline([

('preprocess', preprocess),

('classifier', LogisticRegression(penalty='l2', max_iter=10_000))

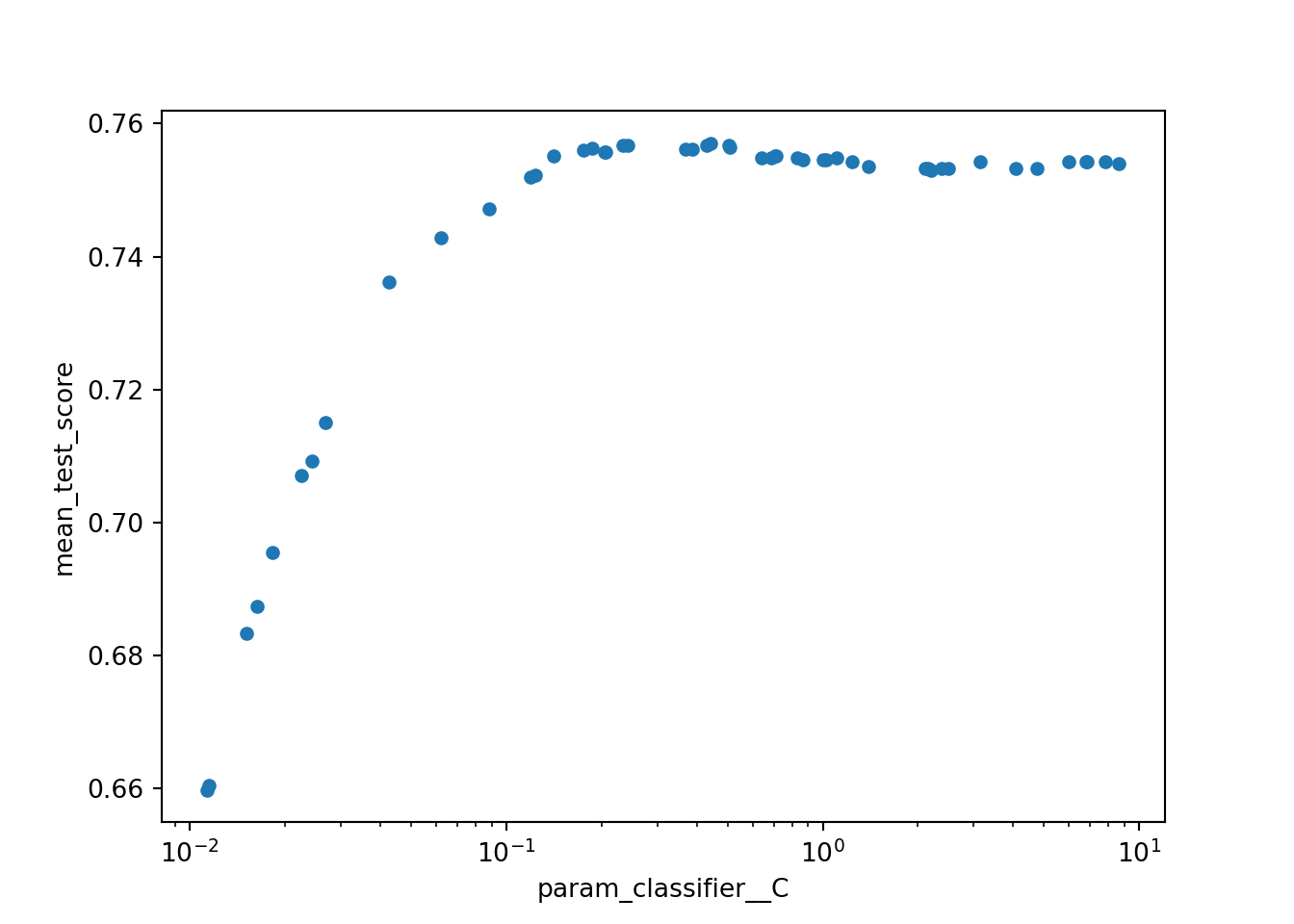

])24.5 Parameter tuning using cross-validation

Code

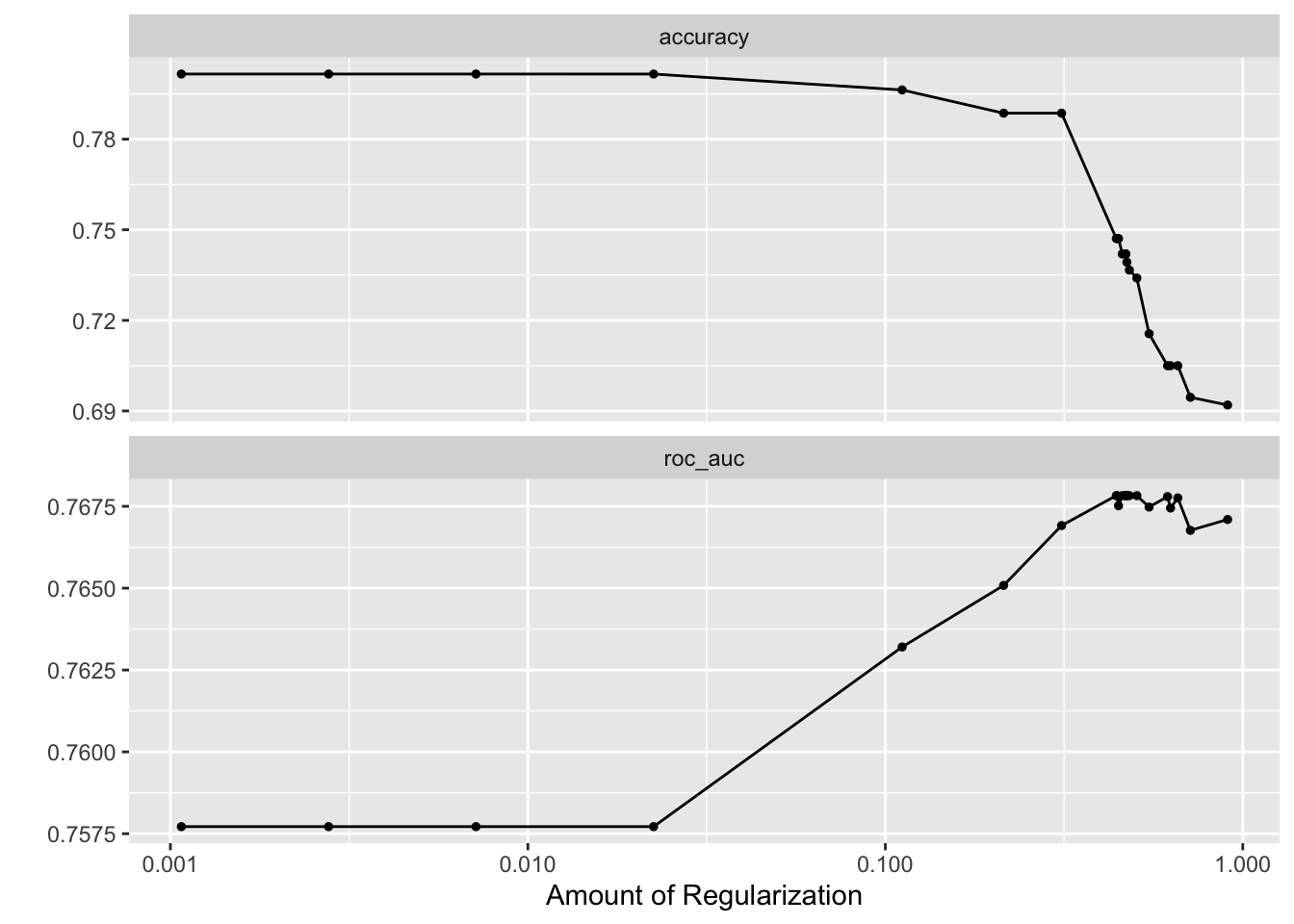

Tune the penalty hyperparameter using Bayesian hyperparameter optimization:

Code

## ! No improvement for 10 iterations; returning current results.

Figure 24.2: Autoplot shows the ROC-AUC for different values of the penalty hyperparameter.

Code

## (np.float64(0.7570491237157904), {'classifier__C': np.float64(0.44303752452182665)})Code

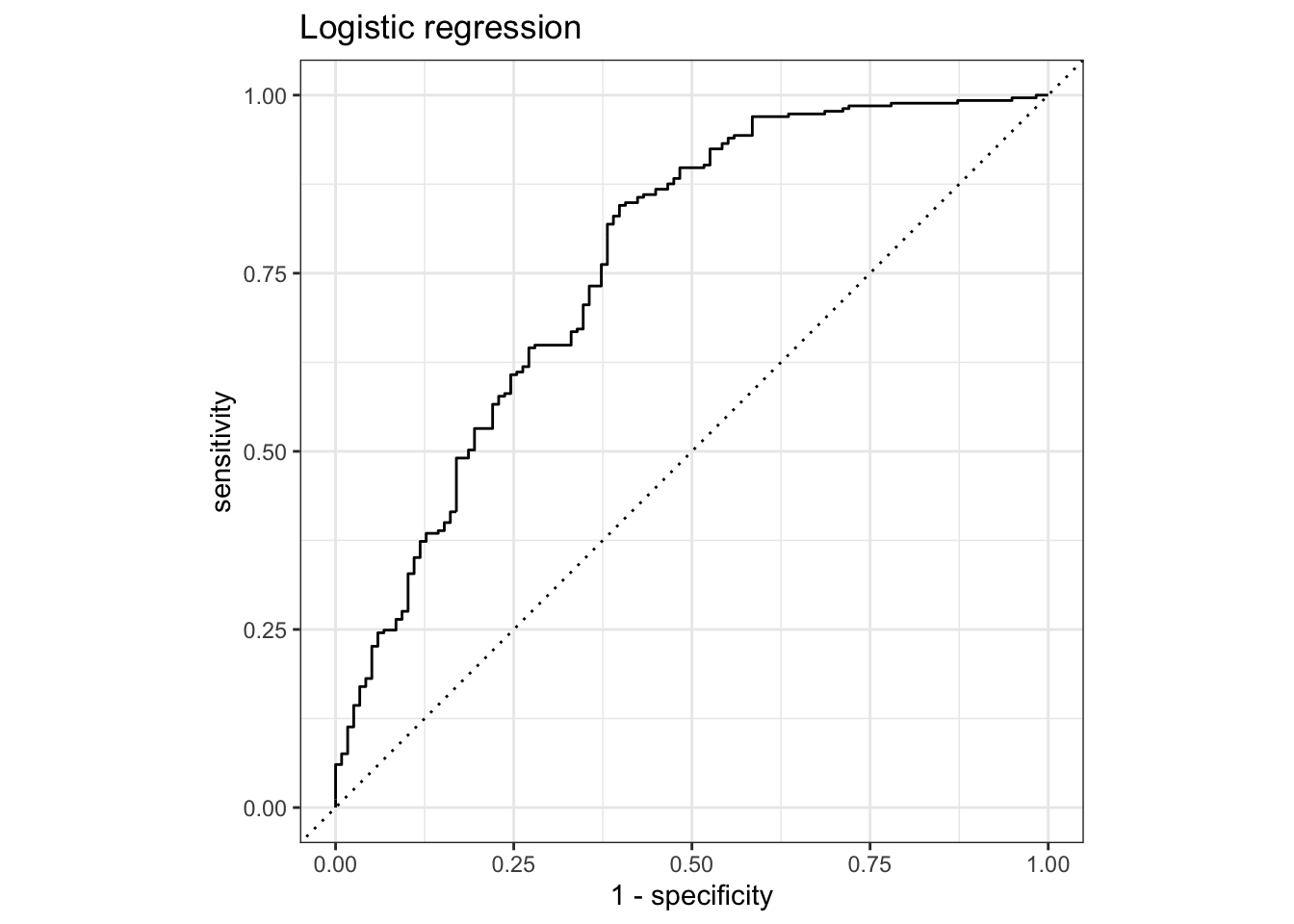

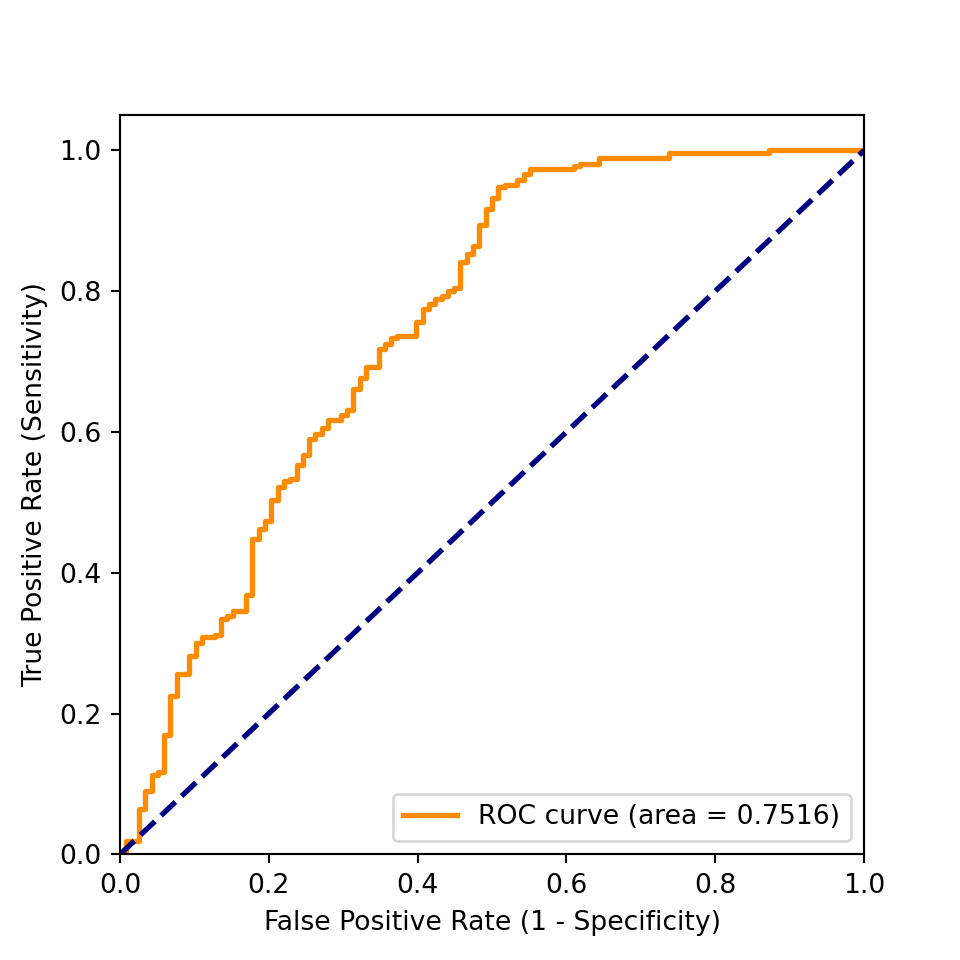

24.6 ROC curves

Code

best_parameter <- select_best(tune_wf, metric="roc_auc")

best_wf <- finalize_workflow(wf, best_parameter)

result_cv <- fit_resamples(best_wf, resamples,

metrics=cv_metrics, control=cv_control)

roc_cv_plot <- function(model_cv, model_name) {

cv_predictions <- collect_predictions(model_cv)

cv_roc <- cv_predictions %>% roc_curve(truth=Loan_Status, .pred_Yes, event_level="second")

autoplot(cv_roc) +

labs(title=model_name)

}

roc_cv_plot(result_cv, "Logistic regression")

Code

from sklearn.metrics import roc_curve, auc

y_train_pred = cross_val_predict(search.best_estimator_, Xtrain, ytrain,

cv=10, method='predict_proba')

fpr, tpr, _ = roc_curve(ytrain, y_train_pred[:, 1])

roc_auc = auc(fpr, tpr)

fig, ax = plt.subplots(figsize=[5, 5])

_ = ax.plot(fpr, tpr, color='darkorange',

lw=2, label=f'ROC curve (area = {roc_auc:0.4f})')

_ = ax.plot([0, 1], [0, 1], color='navy', lw=2, linestyle='--')

_ = ax.set_xlim([0.0, 1.0])

_ = ax.set_ylim([0.0, 1.05])

_ = ax.set_xlabel('False Positive Rate (1 - Specificity)')

_ = ax.set_ylabel('True Positive Rate (Sensitivity)')

_ = ax.legend(loc="lower right")

_ = plt.show()

24.7 Finalize the workflow:

Code

The best roc_auc is obtained with a penalty of best_parameter['penalty'] = 0.4738658.

Use the tuned workflow for cross-validation and training the final model using the full dataset:

Code

Estimate model performance using the cross-validation results and the holdout data:

Code

cv_results <- collect_metrics(result_cv) %>%

select(.metric, mean) %>%

rename(.estimate=mean) %>%

mutate(result="Cross-validation")

holdout_predictions <- augment(fitted_model, new_data=holdout_data)

holdout_results <- bind_rows(

c(roc_auc(holdout_predictions, Loan_Status, .pred_Yes, event_level="second")),

c(accuracy(holdout_predictions, Loan_Status, .pred_class))

) %>%

select(-.estimator) %>%

mutate(result="Holdout")The performance metrics are summarized in the following table.

Code

| result | accuracy | roc_auc |

|---|---|---|

| Cross-validation | 0.739 | 0.768 |

| Holdout | 0.773 | 0.723 |

Python - By default, scikit_learn determines and returns the “best model” after cross-validation.

Code

from sklearn import metrics

best_model = search.best_estimator_

y_holdout_pred = best_model.predict(Xholdout)

pd.DataFrame({

'Accuracy': [

metrics.accuracy_score(ytrain, [1 if p > 0.5 else 0 for p in y_train_pred[:, 1]]),

metrics.accuracy_score(yholdout, y_holdout_pred)],

'ROC AUC': [

metrics.roc_auc_score(ytrain, y_train_pred[:, 1]),

metrics.roc_auc_score(yholdout, best_model.predict_proba(Xholdout)[:, 1])

],

}, index=['Cross-validation', 'Testset'])## Accuracy ROC AUC

## Cross-validation 0.809896 0.751593

## Testset 0.781250 0.715657