Chapter 26 Threshold selection

In this example, we will

- load and preprocess data

- define a workflow

- use cross-validation to determine a threshold using the F-statistic

- train the final model

- evaluate the model using cross-validation and holdout data

- predict

using the Loan prediction dataset to illustrate the whole process.

Load the required packages:

Load and preprocess the data:

Code

data <- read_csv("https://gedeck.github.io/DS-6030/datasets/loan_prediction.csv",

show_col_types=FALSE) %>%

drop_na() %>%

mutate(

Gender=as.factor(Gender),

Married=as.factor(Married),

Dependents=gsub("\\+", "", Dependents) %>% as.numeric(),

Education=as.factor(Education),

Self_Employed=as.factor(Self_Employed),

Credit_History=as.factor(Credit_History),

Property_Area=as.factor(Property_Area),

Loan_Status=factor(Loan_Status, levels=c("N", "Y"), labels=c("No", "Yes"))

) %>%

select(-Loan_ID)Split dataset into training and holdout data, prepare for cross-validation:

Code

set.seed(123)

data_split <- initial_split(data, prop=0.8, strata=Loan_Status)

train_data <- training(data_split)

holdout_data <- testing(data_split)

resamples <- vfold_cv(train_data, v=10, strata=Loan_Status)

cv_metrics <- metric_set(roc_auc, accuracy)

cv_control <- control_resamples(save_pred=TRUE)Define the recipe, the model specification (elasticnet logistic regression), and combine them into a workflow:

Code

formula <- Loan_Status ~ Gender + Married + Dependents + Education + Self_Employed +

ApplicantIncome + CoapplicantIncome + LoanAmount + Loan_Amount_Term +

Credit_History + Property_Area

recipe_spec <- recipe(formula, data=train_data) %>%

step_dummy(all_nominal(), -all_outcomes())

model_spec <- logistic_reg(engine="glm", mode="classification")

wf <- workflow() %>%

add_model(model_spec) %>%

add_recipe(recipe_spec)Use the workflow for cross-validation and training the final model using the full dataset:

Code

Estimate model performance using the cross-validation results and the holdout data:

Code

cv_results <- collect_metrics(result_cv) %>%

select(.metric, mean) %>%

rename(.estimate=mean) %>%

mutate(result="Cross-validation", threshold=0.5)

holdout_predictions <- augment(fitted_model, new_data=holdout_data)

holdout_results <- bind_rows(

c(roc_auc(holdout_predictions, Loan_Status, .pred_Yes, event_level="second")),

c(accuracy(holdout_predictions, Loan_Status, .pred_class))) %>%

select(-.estimator) %>%

mutate(result="Holdout", threshold = 0.5)Code

Code

max_values <- performance %>%

arrange(desc(.threshold)) %>%

group_by(.metric) %>%

filter(.estimate == max(.estimate)) %>%

filter(row_number() == 1)

ggplot(performance, aes(x=.threshold, y=.estimate, color=.metric)) +

geom_line() +

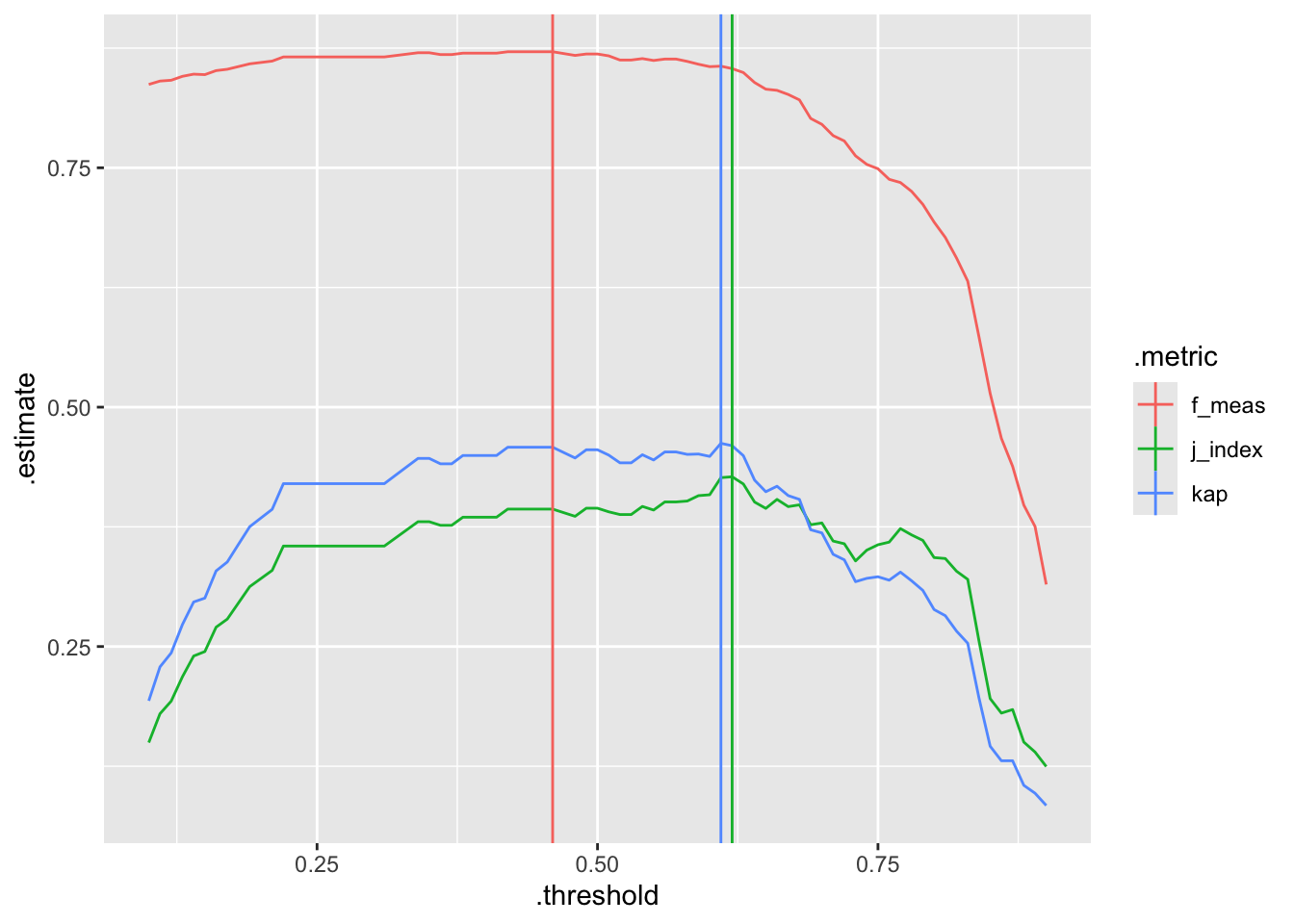

geom_vline(data=max_values, aes(xintercept=.threshold, color=.metric)) We decide to select the threshold that maximizes the F-measure:

We decide to select the threshold that maximizes the F-measure:

We can now calculate the performance metrics using predictions at the selected threshold.

Code

cv_predictions <- collect_predictions(result_cv) %>%

mutate(.pred_class = factor(ifelse(.pred_Yes >= threshold, "Yes", "No")))

cv_threshold_results <- bind_rows(

c(accuracy(cv_predictions, Loan_Status, .pred_class))

) %>%

select(-.estimator) %>%

mutate(result="Cross-validation", threshold=threshold)

holdout_predictions <- augment(fitted_model, new_data=holdout_data) %>%

mutate(.pred_class = factor(ifelse(.pred_Yes >= threshold, "Yes", "No")))

holdout_threshold_results <- bind_rows(

c(accuracy(holdout_predictions, Loan_Status, .pred_class))

) %>%

select(-.estimator) %>%

mutate(result="Holdout", threshold=threshold)The performance metrics are summarized in the following table.

Code

| result | threshold | accuracy | roc_auc |

|---|---|---|---|

| Cross-validation | 0.50 | 0.799 | 0.752 |

| Holdout | 0.50 | 0.825 | 0.733 |

| Cross-validation | 0.46 | 0.802 | NA |

| Holdout | 0.46 | 0.835 | NA |

We can see that the reduced threshold leads to a higher accuracy.