from collections import defaultdict

from itertools import product

from matplotlib.patches import Ellipse

from mlba import plotDecisionTree

from mlba import textDecisionTree

from sklearn import metrics

from sklearn import preprocessing

from sklearn.ensemble import RandomForestClassifier

from sklearn.model_selection import train_test_split

from sklearn.neighbors import KNeighborsClassifier

from sklearn.tree import DecisionTreeClassifier

from xgboost import XGBClassifier

import math

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

import random

import seaborn as sns

random.seed(123)

# Location of the data files. Adjust this path if you keep the data

# files in a different directory.

from pathlib import Path

DATA_DIR = Path('../data')Chapter 6: Statistical Machine Learning

- 2019-2026 Peter C. Bruce, Andrew Bruce, Peter Gedeck

Statistical Machine Learning

K-Nearest Neighbors

A Small Example: Predicting Loan Default

loan200 = pd.read_csv(DATA_DIR / "loan200.csv")

predictors = ["payment_inc_ratio", "dti"]

outcome = "outcome"

newloan = loan200.loc[0:0, predictors]

X = loan200.loc[1:, predictors]

y = loan200.loc[1:, outcome]

knn = KNeighborsClassifier(n_neighbors=20)

knn.fit(X, y)

knn.predict(newloan)array(['paid off'], dtype=object)Standardization (Normalization, z-Scores)

loan_data = pd.read_csv(DATA_DIR / "loan_data.csv.gz")

predictors = ["payment_inc_ratio", "dti", "revol_bal", "revol_util"]

outcome = "outcome"

newloan = loan_data.loc[0:0, predictors]

X = loan_data.loc[1:, predictors]

y = loan_data.loc[1:, outcome]

knn = KNeighborsClassifier(n_neighbors=5)

knn.fit(X, y)

nbrs = knn.kneighbors(newloan)

X.iloc[nbrs[1][0], :]| payment_inc_ratio | dti | revol_bal | revol_util | |

|---|---|---|---|---|

| 35536 | 1.47212 | 1.46 | 1686 | 10.0 |

| 33651 | 3.38178 | 6.37 | 1688 | 8.4 |

| 25863 | 2.36303 | 1.39 | 1691 | 3.5 |

| 42953 | 1.28160 | 7.14 | 1684 | 3.9 |

| 43599 | 4.12244 | 8.98 | 1684 | 7.2 |

newloan = loan_data.loc[0:0, predictors]

X = loan_data.loc[1:, predictors]

y = loan_data.loc[1:, outcome]

scaler = preprocessing.StandardScaler()

scaler.fit(X * 1.0)

X_std = scaler.transform(X * 1.0)

newloan_std = scaler.transform(newloan * 1.0)

knn = KNeighborsClassifier(n_neighbors=5)

knn.fit(X_std, y)

nbrs = knn.kneighbors(newloan_std)

X.iloc[nbrs[1][0], :]| payment_inc_ratio | dti | revol_bal | revol_util | |

|---|---|---|---|---|

| 2080 | 2.61091 | 1.03 | 1218 | 9.7 |

| 1438 | 2.34343 | 0.51 | 278 | 9.9 |

| 30215 | 2.71200 | 1.34 | 1075 | 8.5 |

| 28542 | 2.39760 | 0.74 | 2917 | 7.4 |

| 44737 | 2.34309 | 1.37 | 488 | 7.2 |

KNN as a Feature Engine

predictors = ["dti", "revol_bal", "revol_util", "open_acc",

"delinq_2yrs_zero", "pub_rec_zero"]

outcome = "outcome"

X = loan_data[predictors]

y = loan_data[outcome]

knn = KNeighborsClassifier(n_neighbors=20)

knn.fit(X, y)

loan_data["borrower_score"] = knn.predict_proba(X)[:, 1]

loan_data["borrower_score"].describe()count 45342.000000

mean 0.498901

std 0.128735

min 0.050000

25% 0.400000

50% 0.500000

75% 0.600000

max 1.000000

Name: borrower_score, dtype: float64Tree Models

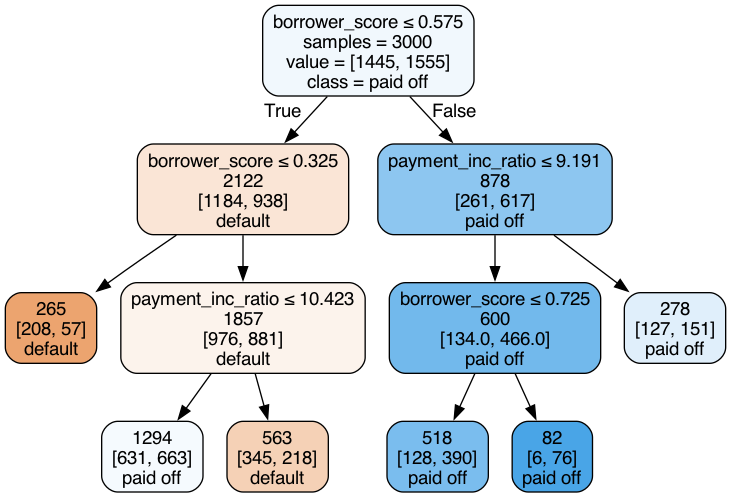

A Simple Example

loan3000 = pd.read_csv(DATA_DIR / "loan3000.csv")

predictors = ["borrower_score", "payment_inc_ratio"]

outcome = "outcome"

X = loan3000[predictors]

y = loan3000[outcome]

loan_tree = DecisionTreeClassifier(random_state=1, criterion="entropy",

min_impurity_decrease=0.003)

loan_tree.fit(X, y)

plotDecisionTree(loan_tree, feature_names=predictors,

class_names=loan_tree.classes_)

print(textDecisionTree(loan_tree))node=0 test node: go to node 1 if 0 <= 0.5750000178813934 else to node 6

node=1 test node: go to node 2 if 0 <= 0.32500000298023224 else to node 3

node=2 leaf node: [[np.float64(0.785), np.float64(0.215)]]

node=3 test node: go to node 4 if 1 <= 10.42264986038208 else to node 5

node=4 leaf node: [[np.float64(0.488), np.float64(0.512)]]

node=5 leaf node: [[np.float64(0.613), np.float64(0.387)]]

node=6 test node: go to node 7 if 1 <= 9.19082498550415 else to node 10

node=7 test node: go to node 8 if 0 <= 0.7249999940395355 else to node 9

node=8 leaf node: [[np.float64(0.247), np.float64(0.753)]]

node=9 leaf node: [[np.float64(0.073), np.float64(0.927)]]

node=10 leaf node: [[np.float64(0.457), np.float64(0.543)]]Bagging and the Random Forest

Random Forest

predictors = ["borrower_score", "payment_inc_ratio"]

outcome = "outcome"

X = loan3000[predictors]

y = loan3000[outcome]

rf = RandomForestClassifier(n_estimators=500, random_state=1, oob_score=True,

n_jobs=4)

rf.fit(X, y)RandomForestClassifier(n_estimators=500, n_jobs=4, oob_score=True,

random_state=1)In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook. On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

Parameters

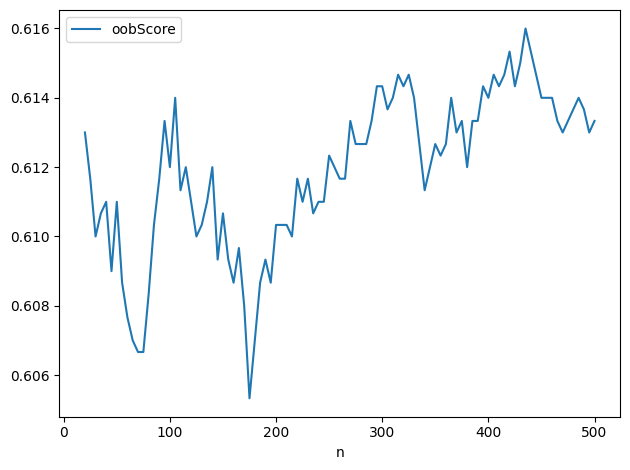

n_estimator = list(range(20, 505, 5))

oob_scores = []

for n in n_estimator:

rf = RandomForestClassifier(n_estimators=n, criterion="entropy", n_jobs=4,

max_depth=5, random_state=1, oob_score=True)

rf.fit(X, y)

oob_scores.append(rf.oob_score_)

df = pd.DataFrame({"n": n_estimator, "oobScore": oob_scores})

df.plot(x="n", y="oobScore")

plt.tight_layout()

plt.show()

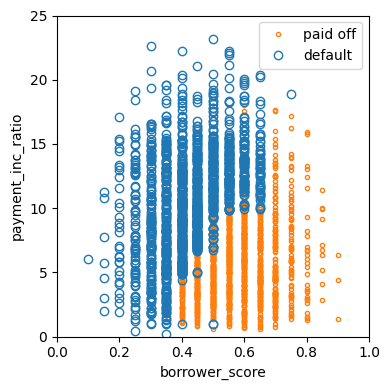

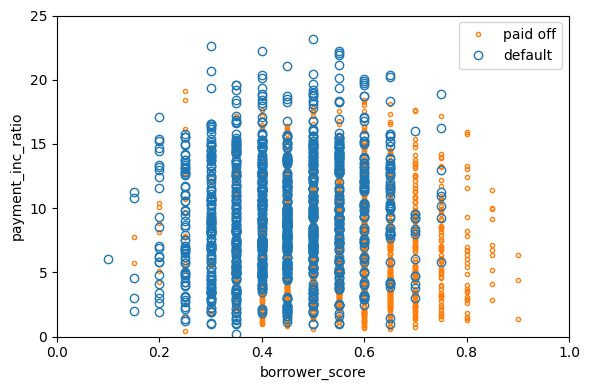

predictions = X.copy()

predictions["prediction"] = rf.predict(X)

predictions.head()

fig, ax = plt.subplots(figsize=(4, 4))

predictions.loc[predictions.prediction == "paid off"].plot(

x="borrower_score", y="payment_inc_ratio", style=".",

markerfacecolor="none", markeredgecolor="C1", ax=ax)

predictions.loc[predictions.prediction == "default"].plot(

x="borrower_score", y="payment_inc_ratio", style="o",

markerfacecolor="none", markeredgecolor="C0", ax=ax)

ax.legend(["paid off", "default"])

ax.set_xlim(0, 1)

ax.set_ylim(0, 25)

ax.set_xlabel("borrower_score")

ax.set_ylabel("payment_inc_ratio")

plt.tight_layout()

plt.show()

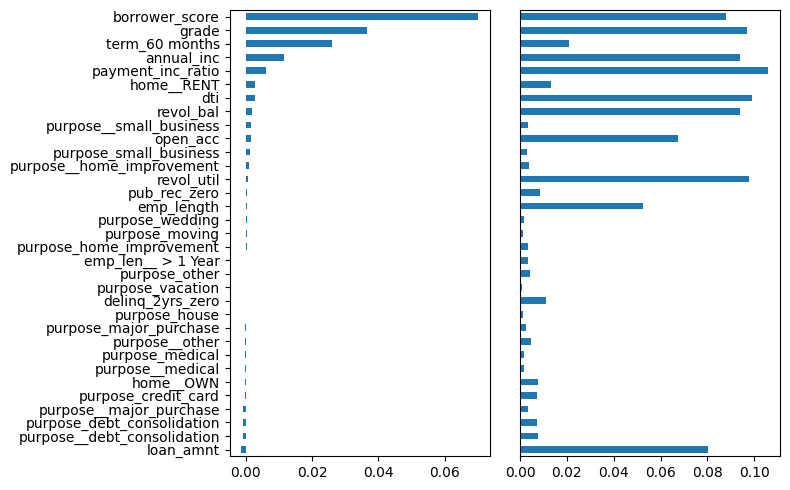

Variable Importance

predictors = ["loan_amnt", "term", "annual_inc", "dti", "payment_inc_ratio",

"revol_bal", "revol_util", "purpose", "delinq_2yrs_zero",

"pub_rec_zero", "open_acc", "grade", "emp_length", "purpose_",

"home_", "emp_len_", "borrower_score"]

outcome = "outcome"

X = pd.get_dummies(loan_data[predictors], drop_first=True)

y = loan_data[outcome]

rf_all = RandomForestClassifier(n_estimators=500, random_state=1, n_jobs=4)

rf_all.fit(X, y)RandomForestClassifier(n_estimators=500, n_jobs=4, random_state=1)In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook.

On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

Parameters

importances = rf_all.feature_importances_rng = np.random.default_rng(seed=321)

rf = RandomForestClassifier(n_estimators=500, n_jobs=4)

scores = defaultdict(list)

# cross-validate the scores on a number of different random splits of the data

for _ in range(3):

train_x, valid_X, train_y, valid_y = train_test_split(X, y, test_size=0.3)

rf.fit(train_x, train_y)

acc = metrics.accuracy_score(valid_y, rf.predict(valid_X))

for column in X.columns:

X_t = valid_X.copy()

X_t[column] = rng.permutation(X_t[column].values)

shuff_acc = metrics.accuracy_score(valid_y, rf.predict(X_t))

scores[column].append((acc - shuff_acc) / acc)df = pd.DataFrame({

"feature": X.columns,

"Accuracy decrease": [np.mean(scores[column]) for column in X.columns],

"Gini decrease": rf_all.feature_importances_,

})

df = df.sort_values("Accuracy decrease")

fig, axes = plt.subplots(ncols=2, figsize=(8, 5))

ax = df.plot(kind="barh", x="feature", y="Accuracy decrease",

legend=False, ax=axes[0])

ax.set_ylabel("")

ax = df.plot(kind="barh", x="feature", y="Gini decrease",

legend=False, ax=axes[1])

ax.set_ylabel("")

ax.get_yaxis().set_visible(False)

plt.tight_layout()

plt.show()

Boosting

XGBoost

predictors = ["borrower_score", "payment_inc_ratio"]

outcome = "outcome"

X = loan3000[predictors]

y = loan3000[outcome]

y = pd.Series([1 if o == "default" else 0 for o in loan3000[outcome]])

xgb = XGBClassifier(objective="binary:logistic", subsample=0.63)

xgb.fit(X, y)XGBClassifier(base_score=None, booster=None, callbacks=None,

colsample_bylevel=None, colsample_bynode=None,

colsample_bytree=None, device=None, early_stopping_rounds=None,

enable_categorical=False, eval_metric=None, feature_types=None,

feature_weights=None, gamma=None, grow_policy=None,

importance_type=None, interaction_constraints=None,

learning_rate=None, max_bin=None, max_cat_threshold=None,

max_cat_to_onehot=None, max_delta_step=None, max_depth=None,

max_leaves=None, min_child_weight=None, missing=nan,

monotone_constraints=None, multi_strategy=None, n_estimators=None,

n_jobs=None, num_parallel_tree=None, ...)In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook. On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

Parameters

xgb_df = X.copy()

xgb_df["prediction"] = ["default" if p == 1 else "paid off"

for p in xgb.predict(X)]

xgb_df["prob_default"] = xgb.predict_proba(X)[:, 0]

fig, ax = plt.subplots(figsize=(6, 4))

xgb_df.loc[xgb_df.prediction == "paid off"].plot(

x="borrower_score", y="payment_inc_ratio", style=".",

markerfacecolor="none", markeredgecolor="C1", ax=ax)

xgb_df.loc[xgb_df.prediction == "default"].plot(

x="borrower_score", y="payment_inc_ratio", style="o",

markerfacecolor="none", markeredgecolor="C0", ax=ax)

ax.legend(["paid off", "default"])

ax.set_xlim(0, 1)

ax.set_ylim(0, 25)

ax.set_xlabel("borrower_score")

ax.set_ylabel("payment_inc_ratio")

plt.tight_layout()

plt.show()

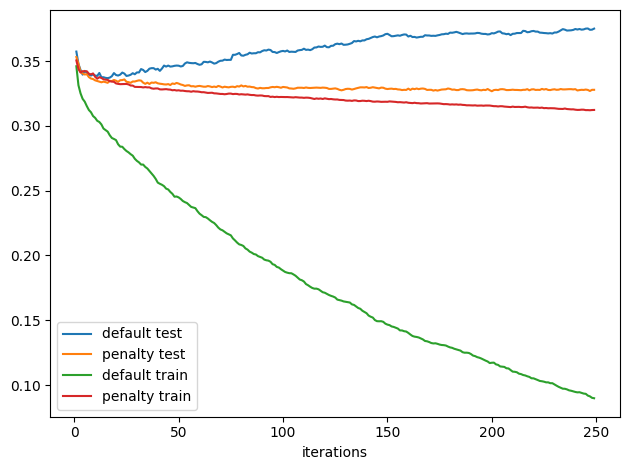

Regularization: Avoiding Overfitting

predictors = ["loan_amnt", "term", "annual_inc", "dti", "payment_inc_ratio",

"revol_bal", "revol_util", "purpose", "delinq_2yrs_zero",

"pub_rec_zero", "open_acc", "grade", "emp_length", "purpose_",

"home_", "emp_len_", "borrower_score"]

outcome = "outcome"

X = pd.get_dummies(loan_data[predictors], drop_first=True)

y = pd.Series([1 if o == "default" else 0 for o in loan_data[outcome]])

train_x, valid_X, train_y, valid_y = train_test_split(X, y, test_size=10000)

xgb_default = XGBClassifier(objective="binary:logistic", n_estimators=250,

max_depth=6, reg_lambda=0, learning_rate=0.3,

subsample=1)

xgb_default.fit(train_x, train_y)

pred_default = xgb_default.predict_proba(valid_X)[:, 1]

error_default = abs(valid_y - pred_default) > 0.5

print("default: ", np.mean(error_default))default: 0.364xgb_penalty = XGBClassifier(objective="binary:logistic", n_estimators=250,

max_depth=6, reg_lambda=1000, learning_rate=0.1,

subsample=0.63)

xgb_penalty.fit(train_x, train_y)

pred_penalty = xgb_penalty.predict_proba(valid_X)[:, 1]

error_penalty = abs(valid_y - pred_penalty) > 0.5

print("penalty: ", np.mean(error_penalty))penalty: 0.3274results = []

for ntree_limit in range(1, 250):

iteration_range = [1, ntree_limit + 1]

train_default = xgb_default.predict_proba(train_x,

iteration_range=iteration_range)[:, 1]

train_penalty = xgb_penalty.predict_proba(train_x,

iteration_range=iteration_range)[:, 1]

pred_default = xgb_default.predict_proba(valid_X,

iteration_range=iteration_range)[:, 1]

pred_penalty = xgb_penalty.predict_proba(valid_X,

iteration_range=iteration_range)[:, 1]

results.append({

"iterations": ntree_limit,

"default train": np.mean(abs(train_y - train_default) > 0.5),

"penalty train": np.mean(abs(train_y - train_penalty) > 0.5),

"default test": np.mean(abs(valid_y - pred_default) > 0.5),

"penalty test": np.mean(abs(valid_y - pred_penalty) > 0.5),

})

results = pd.DataFrame(results)

results.head()| iterations | default train | penalty train | default test | penalty test | |

|---|---|---|---|---|---|

| 0 | 1 | 0.345962 | 0.350490 | 0.3573 | 0.3531 |

| 1 | 2 | 0.331306 | 0.343755 | 0.3477 | 0.3479 |

| 2 | 3 | 0.325081 | 0.341124 | 0.3431 | 0.3415 |

| 3 | 4 | 0.320836 | 0.342199 | 0.3395 | 0.3404 |

| 4 | 5 | 0.318686 | 0.342058 | 0.3424 | 0.3396 |

ax = results.plot(x="iterations", y="default test")

results.plot(x="iterations", y="penalty test", ax=ax)

results.plot(x="iterations", y="default train", ax=ax)

results.plot(x="iterations", y="penalty train", ax=ax)

plt.tight_layout()

plt.show()

Hyperparameters and Cross-Validation

rng = np.random.default_rng(seed=321)

idx = rng.choice(range(5), size=len(X), replace=True)

error = []

for eta, max_depth in product([0.1, 0.5, 0.9], [3, 6, 9]):

xgb = XGBClassifier(objective="binary:logistic", n_estimators=250,

max_depth=max_depth, learning_rate=eta)

cv_error = []

for k in range(5):

fold_idx = idx == k

train_x = X.loc[~fold_idx]; train_y = y[~fold_idx]

valid_X = X.loc[fold_idx]; valid_y = y[fold_idx]

xgb.fit(train_x, train_y)

pred = xgb.predict_proba(valid_X)[:, 1]

cv_error.append(np.mean(abs(valid_y - pred) > 0.5))

error.append({

"eta": eta,

"max_depth": max_depth,

"avg_error": np.mean(cv_error),

})

print(error[-1])

errors = pd.DataFrame(error)

table = errors.pivot_table(index="eta", columns="max_depth", values="avg_error")

print(table * 100){'eta': 0.1, 'max_depth': 3, 'avg_error': np.float64(0.32901685739015657)}

{'eta': 0.1, 'max_depth': 6, 'avg_error': np.float64(0.33584569147367743)}

{'eta': 0.1, 'max_depth': 9, 'avg_error': np.float64(0.3465400449213362)}

{'eta': 0.5, 'max_depth': 3, 'avg_error': np.float64(0.3382451177824208)}

{'eta': 0.5, 'max_depth': 6, 'avg_error': np.float64(0.3693638861385647)}

{'eta': 0.5, 'max_depth': 9, 'avg_error': np.float64(0.3704949129861085)}

{'eta': 0.9, 'max_depth': 3, 'avg_error': np.float64(0.34945523328002775)}

{'eta': 0.9, 'max_depth': 6, 'avg_error': np.float64(0.38570299596812696)}

{'eta': 0.9, 'max_depth': 9, 'avg_error': np.float64(0.3824637201456234)}

max_depth 3 6 9

eta

0.1 32.901686 33.584569 34.654004

0.5 33.824512 36.936389 37.049491

0.9 34.945523 38.570300 38.246372Supplementary Material

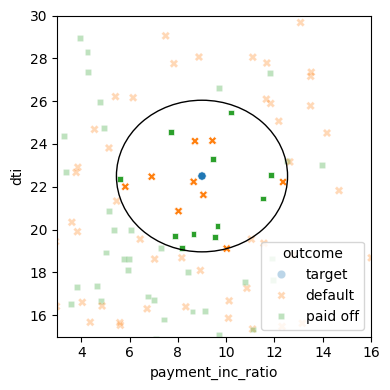

Figure 6-2. KNN prediction of loan default using two variables: debt-to-income ratio and loan-payment-to-income ratio

predictors = ["payment_inc_ratio", "dti"]

outcome = "outcome"

newloan = loan200.loc[0:0, predictors]

X = loan200.loc[1:, predictors]

y = loan200.loc[1:, outcome]

knn = KNeighborsClassifier(n_neighbors=20)

knn.fit(X, y)

nbrs = knn.kneighbors(newloan)

maxDistance = np.max(nbrs[0][0])

fig, ax = plt.subplots(figsize=(4, 4))

sns.scatterplot(x="payment_inc_ratio", y="dti", style="outcome",

hue="outcome", data=loan200, alpha=0.3, ax=ax)

sns.scatterplot(x="payment_inc_ratio", y="dti", style="outcome",

hue="outcome",

data=pd.concat([loan200.loc[0:0, :], loan200.loc[nbrs[1][0] + 1, :]]),

ax=ax, legend=False)

ellipse = Ellipse(xy=newloan.to_numpy()[0],

width=2 * maxDistance, height=2 * maxDistance,

edgecolor="black", fc="None", lw=1)

ax.add_patch(ellipse)

ax.set_xlim(3, 16)

ax.set_ylim(15, 30)

plt.tight_layout()

plt.show()

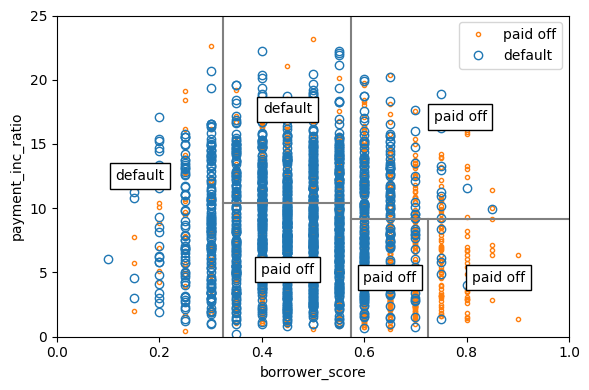

Figure 6-4. The first five rules for a simple tree model fit to the loan data

fig, ax = plt.subplots(figsize=(6, 4))

loan3000.loc[loan3000.outcome == "paid off"].plot(

x="borrower_score", y="payment_inc_ratio", style=".",

markerfacecolor="none", markeredgecolor="C1", ax=ax)

loan3000.loc[loan3000.outcome == "default"].plot(

x="borrower_score", y="payment_inc_ratio", style="o",

markerfacecolor="none", markeredgecolor="C0", ax=ax)

ax.legend(["paid off", "default"])

ax.set_xlim(0, 1)

ax.set_ylim(0, 25)

ax.set_xlabel("borrower_score")

ax.set_ylabel("payment_inc_ratio")

x0 = 0.575

x1a = 0.325; y1b = 9.191

y2a = 10.423; x2b = 0.725

ax.plot((x0, x0), (0, 25), color="grey")

ax.plot((x1a, x1a), (0, 25), color="grey")

ax.plot((x0, 1), (y1b, y1b), color="grey")

ax.plot((x1a, x0), (y2a, y2a), color="grey")

ax.plot((x2b, x2b), (0, y1b), color="grey")

labels = [("default", (x1a / 2, 25 / 2)),

("default", ((x0 + x1a) / 2, (25 + y2a) / 2)),

("paid off", ((x0 + x1a) / 2, y2a / 2)),

("paid off", ((1 + x0) / 2, (y1b + 25) / 2)),

("paid off", ((1 + x2b) / 2, (y1b + 0) / 2)),

("paid off", ((x0 + x2b) / 2, (y1b + 0) / 2)),

]

for label, (x, y) in labels:

ax.text(x, y, label, bbox={"facecolor": "white"},

verticalalignment="center", horizontalalignment="center")

plt.tight_layout()

plt.show()

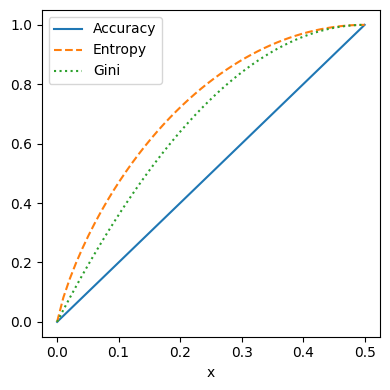

Figure 6-5. Gini impurity and entropy measures

def entropy_function(x):

if x == 0:

return 0

return -x * math.log2(x) - (1 - x) * math.log2(1 - x)

def gini_function(x):

return x * (1 - x)x = np.linspace(0, 0.5, 50)

impure = pd.DataFrame({

"x": x,

"Accuracy": 2 * x,

"Gini": [gini_function(xi) / gini_function(0.5) for xi in x],

"Entropy": [entropy_function(xi) for xi in x],

})

fig, ax = plt.subplots(figsize=(4, 4))

impure.plot(x="x", y="Accuracy", ax=ax, linestyle="solid")

impure.plot(x="x", y="Entropy", ax=ax, linestyle="--")

impure.plot(x="x", y="Gini", ax=ax, linestyle=":")

plt.tight_layout()

plt.show()