# from statsmodels.genmod.generalized_linear_model import GLMResults

from imblearn.over_sampling import SMOTE, ADASYN

from sklearn.compose import ColumnTransformer

from sklearn.discriminant_analysis import LinearDiscriminantAnalysis

from sklearn.linear_model import LogisticRegression

from sklearn.metrics import confusion_matrix

from sklearn.metrics import precision_score, recall_score

from sklearn.metrics import roc_auc_score

from sklearn.metrics import roc_curve

from sklearn.naive_bayes import MultinomialNB

from sklearn.pipeline import Pipeline

from sklearn.preprocessing import OneHotEncoder, KBinsDiscretizer

from sklearn.preprocessing import OrdinalEncoder

from sklearn.tree import DecisionTreeClassifier

import matplotlib.pyplot as plt

import mlba

import numpy as np

import pandas as pd

import pygam

import random

import seaborn as sns

import statsmodels.api as sm

import statsmodels.formula.api as smf

random.seed(123)

# Location of the data files. Adjust this path if you keep the data

# files in a different directory.

from pathlib import Path

DATA_DIR = Path('../data')Chapter 5: Classification

- 2019-2026 Peter C. Bruce, Andrew Bruce, Peter Gedeck

Classification

Naive Bayes

The Naive Solution

loan_data = pd.read_csv(DATA_DIR / "loan_data.csv.gz")

predictors = ["purpose_", "home_", "emp_len_"]

outcome = "outcome"

X = pd.get_dummies(loan_data[predictors], prefix="", prefix_sep="", dtype=int)

y = loan_data[outcome]

naive_model = MultinomialNB(alpha=0.01, fit_prior=True)

naive_model.fit(X, y)MultinomialNB(alpha=0.01)In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook.

On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

Parameters

new_loan = X.loc[146:146, :]print("predicted class: ", naive_model.predict(new_loan)[0])

probabilities = pd.DataFrame(naive_model.predict_proba(new_loan),

columns=naive_model.classes_)

print("predicted probabilities", probabilities)predicted class: default

predicted probabilities default paid off

0 0.653696 0.346304Numeric Predictor Variables

num_cols = ["borrower_score", "payment_inc_ratio"]

cat_cols = ["purpose_", "home_", "emp_len_"]

mixed_naive_model = Pipeline([

("pre", ColumnTransformer([

("cat", OneHotEncoder(handle_unknown="ignore"), cat_cols),

("num", KBinsDiscretizer(n_bins=5, strategy="uniform"), num_cols),

])),

("clf", MultinomialNB()),

])

X = loan_data[cat_cols + num_cols]

mixed_naive_model.fit(X, loan_data["outcome"])Pipeline(steps=[('pre',

ColumnTransformer(transformers=[('cat',

OneHotEncoder(handle_unknown='ignore'),

['purpose_', 'home_',

'emp_len_']),

('num',

KBinsDiscretizer(strategy='uniform'),

['borrower_score',

'payment_inc_ratio'])])),

('clf', MultinomialNB())])In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook. On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

Parameters

Parameters

['purpose_', 'home_', 'emp_len_']

Parameters

['borrower_score', 'payment_inc_ratio']

Parameters

Parameters

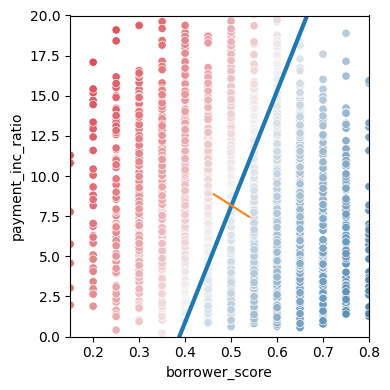

Discriminant Analysis

A Simple Example

loan3000 = pd.read_csv(DATA_DIR / "loan3000.csv")

loan3000.outcome = loan3000.outcome.astype("category")

predictors = ["borrower_score", "payment_inc_ratio"]

outcome = "outcome"

X = loan3000[predictors]

y = loan3000[outcome]

loan_lda = LinearDiscriminantAnalysis()

loan_lda.fit(X, y)

pd.DataFrame(loan_lda.scalings_, index=X.columns)| 0 | |

|---|---|

| borrower_score | 7.175839 |

| payment_inc_ratio | -0.099676 |

pred = pd.DataFrame(loan_lda.predict_proba(loan3000[predictors]),

columns=loan_lda.classes_)

pred.head()| default | paid off | |

|---|---|---|

| 0 | 0.553544 | 0.446456 |

| 1 | 0.558953 | 0.441047 |

| 2 | 0.272696 | 0.727304 |

| 3 | 0.506254 | 0.493746 |

| 4 | 0.609952 | 0.390048 |

# Use scalings and center of means to determine decision boundary

center = np.mean(loan_lda.means_, axis=0)

slope = - loan_lda.scalings_[0] / loan_lda.scalings_[1]

intercept = center[1] - center[0] * slope

# payment_inc_ratio for borrower_score of 0 and 20

x_0 = (0 - intercept) / slope

x_20 = (20 - intercept) / slope

lda_df = pd.concat([loan3000, pred["default"]], axis=1)

lda_df.head()

fig, ax = plt.subplots(figsize=(4, 4))

g = sns.scatterplot(x="borrower_score", y="payment_inc_ratio",

hue="default", data=lda_df,

palette=sns.diverging_palette(240, 10, n=9, as_cmap=True),

ax=ax, legend=False)

ax.set_ylim(0, 20)

ax.set_xlim(0.15, 0.8)

ax.plot((x_0, x_20), (0, 20), linewidth=3)

ax.plot(*loan_lda.means_.transpose())

plt.tight_layout()

plt.show()

Logistic Regression

Logistic Regression and the GLM

predictors = ["payment_inc_ratio", "purpose_", "home_", "emp_len_",

"borrower_score"]

outcome = "outcome"

X = pd.get_dummies(loan_data[predictors], prefix="", prefix_sep="",

drop_first=True, dtype=int)

y = loan_data[outcome]

logit_reg = LogisticRegression(C=np.inf, max_iter=1000)

logit_reg.fit(X, y)/Users/petergedeck/cdd/practical-statistics-for-data-scientists-code-3e/.venv/lib/python3.13/site-packages/sklearn/linear_model/_logistic.py:1170: UserWarning: Setting penalty=None will ignore the C and l1_ratio parameters

warnings.warn(LogisticRegression(C=inf, max_iter=1000)In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook.

On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

Parameters

print("intercept ", logit_reg.intercept_[0])

print("classes", logit_reg.classes_)

pd.DataFrame({"coeff": logit_reg.coef_[0]}, index=X.columns)intercept -1.6261242575653818

classes ['default' 'paid off']| coeff | |

|---|---|

| payment_inc_ratio | -0.079885 |

| borrower_score | 4.610744 |

| debt_consolidation | -0.250128 |

| home_improvement | -0.411826 |

| major_purchase | -0.228901 |

| medical | -0.528521 |

| other | -0.620839 |

| small_business | -1.222285 |

| OWN | -0.052460 |

| RENT | -0.159205 |

| > 1 Year | 0.349254 |

Predicted Values from Logistic Regression

pred = pd.DataFrame(logit_reg.predict_log_proba(X),

columns=logit_reg.classes_)

pred.describe()| default | paid off | |

|---|---|---|

| count | 45342.000000 | 45342.000000 |

| mean | -0.758078 | -0.760365 |

| std | 0.378317 | 0.390689 |

| min | -2.771842 | -3.546430 |

| 25% | -0.986107 | -0.977608 |

| 50% | -0.697477 | -0.688836 |

| 75% | -0.471941 | -0.466850 |

| max | -0.029251 | -0.064588 |

pred = pd.DataFrame(logit_reg.predict_proba(X),

columns=logit_reg.classes_)

pred.describe()| default | paid off | |

|---|---|---|

| count | 45342.000000 | 45342.000000 |

| mean | 0.499934 | 0.500066 |

| std | 0.167427 | 0.167427 |

| min | 0.062547 | 0.028827 |

| 25% | 0.373026 | 0.376210 |

| 50% | 0.497840 | 0.502160 |

| 75% | 0.623790 | 0.626974 |

| max | 0.971173 | 0.937453 |

Assessing the Model

y_numbers = [1 if yi == "default" else 0 for yi in y]

logit_reg_sm = sm.GLM(y_numbers, X.assign(const=1),

family=sm.families.Binomial())

logit_result = logit_reg_sm.fit()

print(logit_result.summary()) Generalized Linear Model Regression Results

==============================================================================

Dep. Variable: y No. Observations: 45342

Model: GLM Df Residuals: 45330

Model Family: Binomial Df Model: 11

Link Function: Logit Scale: 1.0000

Method: IRLS Log-Likelihood: -28757.

Date: Sun, 31 May 2026 Deviance: 57515.

Time: 18:07:11 Pearson chi2: 4.54e+04

No. Iterations: 4 Pseudo R-squ. (CS): 0.1112

Covariance Type: nonrobust

======================================================================================

coef std err z P>|z| [0.025 0.975]

--------------------------------------------------------------------------------------

payment_inc_ratio 0.0797 0.002 32.058 0.000 0.075 0.085

borrower_score -4.6126 0.084 -55.203 0.000 -4.776 -4.449

debt_consolidation 0.2494 0.028 9.030 0.000 0.195 0.303

home_improvement 0.4077 0.047 8.747 0.000 0.316 0.499

major_purchase 0.2296 0.054 4.277 0.000 0.124 0.335

medical 0.5105 0.087 5.882 0.000 0.340 0.681

other 0.6207 0.039 15.738 0.000 0.543 0.698

small_business 1.2153 0.063 19.192 0.000 1.091 1.339

OWN 0.0483 0.038 1.271 0.204 -0.026 0.123

RENT 0.1573 0.021 7.420 0.000 0.116 0.199

> 1 Year -0.3567 0.053 -6.779 0.000 -0.460 -0.254

const 1.6381 0.074 22.224 0.000 1.494 1.783

======================================================================================formula = ("outcome ~ bs(payment_inc_ratio, df=4) + purpose_ + "

"home_ + emp_len_ + bs(borrower_score, df=4)")

model = smf.glm(formula=formula, data=loan_data, family=sm.families.Binomial())

results = model.fit()print(results.summary()) Generalized Linear Model Regression Results

=====================================================================================================

Dep. Variable: ['outcome[default]', 'outcome[paid off]'] No. Observations: 45342

Model: GLM Df Residuals: 45324

Model Family: Binomial Df Model: 17

Link Function: Logit Scale: 1.0000

Method: IRLS Log-Likelihood: -28744.

Date: Sun, 31 May 2026 Deviance: 57487.

Time: 18:07:11 Pearson chi2: 4.54e+04

No. Iterations: 5 Pseudo R-squ. (CS): 0.1117

Covariance Type: nonrobust

==================================================================================================

coef std err z P>|z| [0.025 0.975]

--------------------------------------------------------------------------------------------------

Intercept 1.8382 0.380 4.836 0.000 1.093 2.583

purpose_[T.debt_consolidation] 0.2491 0.028 9.020 0.000 0.195 0.303

purpose_[T.home_improvement] 0.4138 0.047 8.848 0.000 0.322 0.505

purpose_[T.major_purchase] 0.2401 0.054 4.450 0.000 0.134 0.346

purpose_[T.medical] 0.5183 0.087 5.953 0.000 0.348 0.689

purpose_[T.other] 0.6295 0.040 15.812 0.000 0.552 0.708

purpose_[T.small_business] 1.2252 0.063 19.303 0.000 1.101 1.350

home_[T.OWN] 0.0484 0.038 1.273 0.203 -0.026 0.123

home_[T.RENT] 0.1581 0.021 7.456 0.000 0.117 0.200

emp_len_[T. > 1 Year] -0.3541 0.053 -6.729 0.000 -0.457 -0.251

bs(payment_inc_ratio, df=4)[0] 0.0049 0.121 0.041 0.967 -0.232 0.241

bs(payment_inc_ratio, df=4)[1] 1.6033 0.142 11.289 0.000 1.325 1.882

bs(payment_inc_ratio, df=4)[2] 1.9033 0.488 3.900 0.000 0.947 2.860

bs(payment_inc_ratio, df=4)[3] -0.8521 1.929 -0.442 0.659 -4.633 2.929

bs(borrower_score, df=4)[0] -1.0045 0.476 -2.112 0.035 -1.937 -0.072

bs(borrower_score, df=4)[1] -2.6411 0.287 -9.209 0.000 -3.203 -2.079

bs(borrower_score, df=4)[2] -3.6984 0.473 -7.824 0.000 -4.625 -2.772

bs(borrower_score, df=4)[3] -5.8564 0.525 -11.160 0.000 -6.885 -4.828

==================================================================================================Analysis of residuals

Evaluating Classification Models

Confusion Matrix

pred = logit_reg.predict(X)

pred_y = logit_reg.predict(X) == "default"

true_y = y == "default"

true_pos = true_y & pred_y

true_neg = ~true_y & ~pred_y

false_pos = ~true_y & pred_y

false_neg = true_y & ~pred_y

conf_mat = pd.DataFrame([[np.sum(true_pos), np.sum(false_neg)],

[np.sum(false_pos), np.sum(true_neg)]],

index=["Y = default", "Y = paid off"],

columns=["Yhat = default", "Yhat = paid off"])

conf_mat| Yhat = default | Yhat = paid off | |

|---|---|---|

| Y = default | 14321 | 8350 |

| Y = paid off | 8140 | 14531 |

print(confusion_matrix(y_true=y, y_pred=logit_reg.predict(X)))[[14321 8350]

[ 8140 14531]]mlba.classificationSummary(y_true=y, y_pred=logit_reg.predict(X))Confusion Matrix (Accuracy 0.6363)

Prediction

Actual default paid off

default 14321 8350

paid off 8140 14531Precision, Recall, and Specificity

y_pred = logit_reg.predict(X)

print("precision ", precision_score(y, y_pred, pos_label="default"))

print("recall. ", recall_score(y, y_pred, pos_label="default"))

print("specificity", recall_score(y, y_pred, pos_label="paid off"))precision 0.6375940519122034

recall. 0.6316880596356579

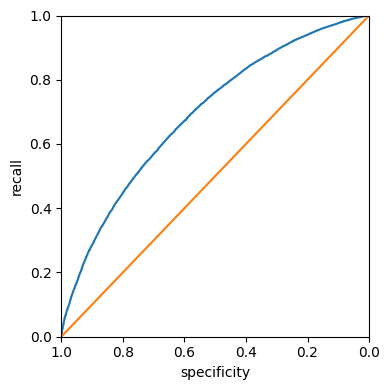

specificity 0.640950994662785ROC Curve

fpr, tpr, thresholds = roc_curve(y, logit_reg.predict_proba(X)[:, 0],

pos_label="default")

roc_df = pd.DataFrame({"recall": tpr, "specificity": 1 - fpr})

ax = roc_df.plot(x="specificity", y="recall", figsize=(4, 4), legend=False)

ax.set_ylim(0, 1)

ax.set_xlim(1, 0)

ax.plot((1, 0), (0, 1))

ax.set_xlabel("specificity")

ax.set_ylabel("recall")

plt.tight_layout()

plt.show()

AUC

print(np.sum(roc_df.recall[:-1] * np.diff(1 - roc_df.specificity)))

print(roc_auc_score([1 if yi == "default" else 0 for yi in y],

logit_reg.predict_proba(X)[:, 0]))0.6917057288869074

0.6917058067118191Strategies for Imbalanced Data

Undersampling

full_train_set = pd.read_csv(DATA_DIR / "full_train_set.csv.gz")

print("percentage of loans in default: ",

100 * np.mean(full_train_set.outcome == "default"))percentage of loans in default: 18.894546909248504predictors = ["payment_inc_ratio", "purpose_", "home_", "emp_len_",

"dti", "revol_bal", "revol_util"]

outcome = "outcome"

X = pd.get_dummies(full_train_set[predictors], prefix="", prefix_sep="",

drop_first=True, dtype=int)

y = full_train_set[outcome]

full_model = LogisticRegression(C=np.inf, max_iter=10_000)

full_model.fit(X, y)

print("percentage of loans predicted to default: ",

100 * np.mean(full_model.predict(X) == "default"))/Users/petergedeck/cdd/practical-statistics-for-data-scientists-code-3e/.venv/lib/python3.13/site-packages/sklearn/linear_model/_logistic.py:1170: UserWarning: Setting penalty=None will ignore the C and l1_ratio parameters

warnings.warn(percentage of loans predicted to default: 0.3883754073357947Oversampling and Up/Down Weighting

default_wt = 1 / np.mean(full_train_set.outcome == "default")

wt = [default_wt if outcome == "default" else 1

for outcome in full_train_set.outcome]

full_model = LogisticRegression(C=np.inf, max_iter=10_000)

full_model.fit(X, y, sample_weight=wt)

print("percentage of loans predicted to default (weighting): ",

100 * np.mean(full_model.predict(X) == "default"))/Users/petergedeck/cdd/practical-statistics-for-data-scientists-code-3e/.venv/lib/python3.13/site-packages/sklearn/linear_model/_logistic.py:1170: UserWarning: Setting penalty=None will ignore the C and l1_ratio parameters

warnings.warn(percentage of loans predicted to default (weighting): 57.61874203038663Supplementary Material

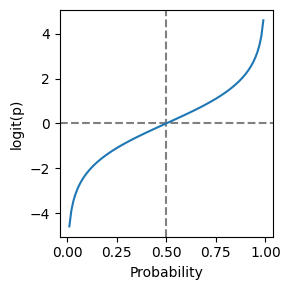

Figure 5-2. Graph of the logit function that maps a probability to a scale suitable for a linear model

p = np.arange(0.01, 1, 0.01)

df = pd.DataFrame({

"p": p,

"logit": np.log(p / (1 - p)),

"odds": p / (1 - p),

})

fig, ax = plt.subplots(figsize=(3, 3))

ax.axhline(0, color="grey", linestyle="--")

ax.axvline(0.5, color="grey", linestyle="--")

ax.plot(df["p"], df["logit"])

ax.set_xlabel("Probability")

ax.set_ylabel("logit(p)")

plt.tight_layout()

plt.show()

How to control the order of the classes in Python

# If you have a feature or outcome variable that is ordinal, use

# the scikit-learn `OrdinalEncoder` to replace the categories

# (here, "paid off" and "default") with numbers. In the below code,

# we replace "paid off" with 0 and "default" with 1. This reverses

# the order of the predicted classes and as a consequence, the

# coefficients will be reversed. You will however now need to

# keep track of how the the numbers map back to the classes.predictors = ["payment_inc_ratio", "purpose_", "home_", "emp_len_",

"borrower_score"]

outcome = "outcome"

X = pd.get_dummies(loan_data[predictors], prefix="", prefix_sep="",

drop_first=True, dtype=int)

enc = OrdinalEncoder(categories=[["paid off", "default"]])

y_enc = enc.fit_transform(loan_data[[outcome]]).ravel()

logit_reg_enc = LogisticRegression(C=np.inf, max_iter=1000)

logit_reg_enc.fit(X, y_enc)

print("intercept ", logit_reg_enc.intercept_[0])

print("classes", logit_reg_enc.classes_)

pd.DataFrame({"coeff": logit_reg_enc.coef_[0]}, index=X.columns)intercept 1.6262802328204813

classes [0. 1.]/Users/petergedeck/cdd/practical-statistics-for-data-scientists-code-3e/.venv/lib/python3.13/site-packages/sklearn/linear_model/_logistic.py:1170: UserWarning: Setting penalty=None will ignore the C and l1_ratio parameters

warnings.warn(| coeff | |

|---|---|

| payment_inc_ratio | 0.079896 |

| borrower_score | -4.611003 |

| debt_consolidation | 0.250206 |

| home_improvement | 0.411879 |

| major_purchase | 0.228987 |

| medical | 0.528678 |

| other | 0.620869 |

| small_business | 1.222274 |

| OWN | 0.052453 |

| RENT | 0.159220 |

| > 1 Year | -0.349459 |

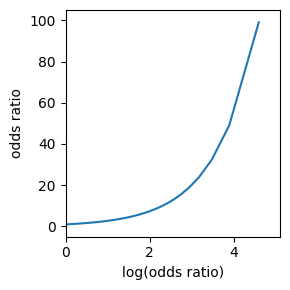

Figure 5-3. The relationship between the odds ratio and the log-odds ratio

fig, ax = plt.subplots(figsize=(3, 3))

ax.plot(df["logit"], df["odds"])

ax.set_xlabel("log(odds ratio)")

ax.set_ylabel("odds ratio")

ax.set_xlim(0, 5.1)

ax.set_ylim(-5, 105)

plt.tight_layout()

plt.show()

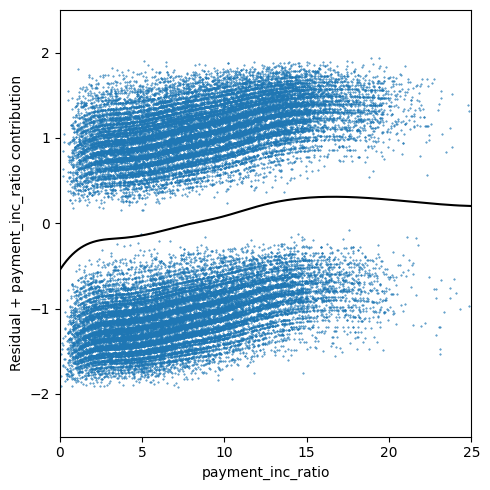

Figure 5-4. Partial residuals from logistic regression

def partial_residual_plot(model, df, outcome, feature, fig, ax):

y_actual = [0 if s == "default" else 1 for s in df[outcome]]

y_pred = model.predict(df)

org_params = model.params.copy()

zero_params = model.params.copy()

# set model parametes of other features to 0

for i, name in enumerate(zero_params.index):

if feature in name:

continue

zero_params.iloc[i] = 0.0

model.initialize(model.model, zero_params)

feature_prediction = model.predict(df)

ypartial = -np.log(1 / feature_prediction - 1)

ypartial -= np.mean(ypartial)

model.initialize(model.model, org_params)

results = pd.DataFrame({

"feature": df[feature],

"residual": -2 * (y_actual - y_pred),

"ypartial": ypartial / 2,

})

results = results.sort_values(by=["feature"])

ax.scatter(results.feature, results.residual, marker=".", s=72. / fig.dpi)

ax.plot(results.feature, results.ypartial, color="black")

ax.set_xlabel(feature)

ax.set_ylabel(f"Residual + {feature} contribution")

return ax

formula = ("outcome ~ bs(payment_inc_ratio, df=8) + purpose_ + "

"home_ + emp_len_ + bs(borrower_score, df=3)")

model = smf.glm(formula=formula, data=loan_data, family=sm.families.Binomial())

results = model.fit()

fig, ax = plt.subplots(figsize=(5, 5))

partial_residual_plot(results, loan_data, "outcome", "payment_inc_ratio", fig, ax)

ax.set_xlim(0, 25)

ax.set_ylim(-2.5, 2.5)

plt.tight_layout()

plt.show()

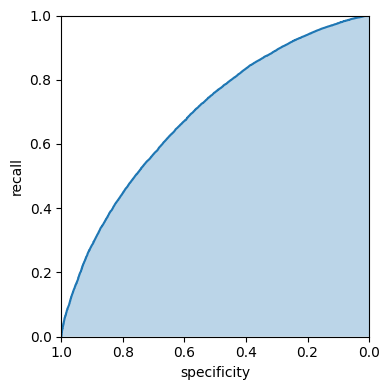

Figure 5-7. Area under the ROC curve for the loan data

ax = roc_df.plot(x="specificity", y="recall", figsize=(4, 4), legend=False)

ax.set_ylim(0, 1)

ax.set_xlim(1, 0)

ax.set_xlabel("specificity")

ax.set_ylabel("recall")

ax.fill_between(roc_df.specificity, 0, roc_df.recall, alpha=0.3)

plt.tight_layout()

plt.show()

SMOTE

predictors = ["payment_inc_ratio", "purpose_", "home_", "emp_len_",

"dti", "revol_bal", "revol_util"]

outcome = "outcome"

X = pd.get_dummies(full_train_set[predictors], prefix="", prefix_sep="",

drop_first=True, dtype=int)

y = full_train_set[outcome]

X_resampled, y_resampled = SMOTE().fit_resample(X, y)

print("percentage of loans in default (SMOTE resampled): ",

f"{100 * np.mean(y_resampled == 'default'):.2f}")

full_model = LogisticRegression(C=np.inf, max_iter=10_000)

full_model.fit(X_resampled, y_resampled)

print("percentage of loans predicted to default (SMOTE): ",

f"{100 * np.mean(full_model.predict(X) == 'default'):.2f}")

X_resampled, y_resampled = ADASYN().fit_resample(X, y)

print("percentage of loans in default (ADASYN resampled): ",

f"{100 * np.mean(y_resampled == 'default'):.2f}")

full_model = LogisticRegression(C=np.inf, max_iter=10_000)

full_model.fit(X_resampled, y_resampled)

print("percentage of loans predicted to default (ADASYN): ",

f"{100 * np.mean(full_model.predict(X) == 'default'):.2f}")percentage of loans in default (SMOTE resampled): 50.00/Users/petergedeck/cdd/practical-statistics-for-data-scientists-code-3e/.venv/lib/python3.13/site-packages/sklearn/linear_model/_logistic.py:1170: UserWarning: Setting penalty=None will ignore the C and l1_ratio parameters

warnings.warn(percentage of loans predicted to default (SMOTE): 29.51

percentage of loans in default (ADASYN resampled): 48.56/Users/petergedeck/cdd/practical-statistics-for-data-scientists-code-3e/.venv/lib/python3.13/site-packages/sklearn/linear_model/_logistic.py:1170: UserWarning: Setting penalty=None will ignore the C and l1_ratio parameters

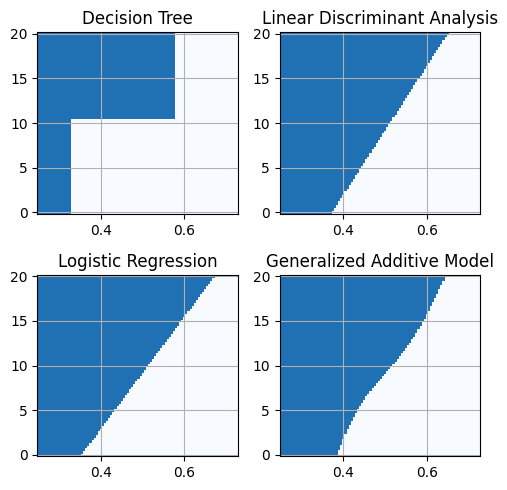

warnings.warn(percentage of loans predicted to default (ADASYN): 27.37Figure 5-8. Comparison of the classification rules for four different methods

predictors = ["borrower_score", "payment_inc_ratio"]

outcome = "outcome"

X = loan3000[predictors]

y = loan3000[outcome]

loan_tree = DecisionTreeClassifier(random_state=1, criterion="entropy",

min_impurity_decrease=0.003)

loan_tree.fit(X, y)

loan_lda = LinearDiscriminantAnalysis()

loan_lda.fit(X, y)

logit_reg = LogisticRegression(penalty="l2", solver="liblinear")

logit_reg.fit(X, y)

## model

gam = pygam.LinearGAM(pygam.s(0) + pygam.s(1))

print(gam.gridsearch(X.values, [1 if yi == "default" else 0 for yi in y]))/Users/petergedeck/cdd/practical-statistics-for-data-scientists-code-3e/.venv/lib/python3.13/site-packages/sklearn/linear_model/_logistic.py:1135: FutureWarning: 'penalty' was deprecated in version 1.8 and will be removed in 1.10. To avoid this warning, leave 'penalty' set to its default value and use 'l1_ratio' or 'C' instead. Use l1_ratio=0 instead of penalty='l2', l1_ratio=1 instead of penalty='l1', and C=np.inf instead of penalty=None. warnings.warn( 0% (0 of 11) | | Elapsed Time: 0:00:00 ETA: --:--:-- 45% (5 of 11) |########### | Elapsed Time: 0:00:00 ETA: 0:00:00 90% (10 of 11) |##################### | Elapsed Time: 0:00:00 ETA: 0:00:00 100% (11 of 11) |########################| Elapsed Time: 0:00:00 Time: 0:00:00

LinearGAM(callbacks=[Deviance(), Diffs()], fit_intercept=True,

max_iter=100, scale=None, terms=s(0) + s(1) + intercept,

tol=0.0001, verbose=False)models = {

"Decision Tree": loan_tree,

"Linear Discriminant Analysis": loan_lda,

"Logistic Regression": logit_reg,

"Generalized Additive Model": gam,

}

fig, axes = plt.subplots(nrows=2, ncols=2, figsize=(5, 5))

xvalues = np.arange(0.25, 0.73, 0.005)

yvalues = np.arange(-0.1, 20.1, 0.1)

xx, yy = np.meshgrid(xvalues, yvalues)

X = pd.DataFrame({

"borrower_score": xx.ravel(),

"payment_inc_ratio": yy.ravel(),

})

boundary = {}

for n, (title, model) in enumerate(models.items()):

ax = axes[n // 2, n % 2]

predict = model.predict(X)

if "Generalized" in title:

Z = np.array([1 if z > 0.5 else 0 for z in predict])

else:

Z = np.array([1 if z == "default" else 0 for z in predict])

Z = Z.reshape(xx.shape)

boundary[title] = yvalues[np.argmax(Z > 0, axis=0)]

boundary[title][Z[-1, :] == 0] = yvalues[-1]

c = ax.pcolormesh(xx, yy, Z, cmap="Blues", vmin=0.1, vmax=1.3, shading="auto")

ax.set_title(title)

ax.grid(visible=True)

plt.tight_layout()

plt.show()