library(tidyverse)

library(tidymodels)28 Threshold selection with tuning

In this example, we will

- load and preprocess data

- define a workflow including a tunable threshold

- tune the threshold using cross-validation and the F-measure

- train the final model

- evaluate the model using cross-validation and holdout data

using the Loan prediction dataset to illustrate the whole process.

Load the required packages:

Load and preprocess the data:

filename <- paste0(

"https://gedeck.github.io/machine-learning-with-tidymodels/",

"datasets/loan_prediction.csv"

)

data <- read_csv(filename, show_col_types = FALSE) |>

drop_na() |>

mutate(

Gender = as.factor(Gender),

Married = as.factor(Married),

Dependents = gsub("\\+", "", Dependents) |> as.numeric(),

Education = as.factor(Education),

Self_Employed = as.factor(Self_Employed),

Credit_History = as.factor(Credit_History),

Property_Area = as.factor(Property_Area),

Loan_Status = factor(Loan_Status, levels = c("Y", "N"),

labels = c("Yes", "No"))

) |>

select(-Loan_ID)Split dataset into training and holdout data, prepare for cross-validation:

set.seed(123)

data_split <- initial_split(data, prop = 0.8, strata = Loan_Status)

train_data <- training(data_split)

holdout_data <- testing(data_split)

resamples <- vfold_cv(train_data, v = 10, strata = Loan_Status)

cv_metrics <- metric_set(f_meas, roc_auc, accuracy)

cv_control <- control_resamples(save_pred = TRUE)Define the recipe, the model specification (elasticnet logistic regression), and combine them into a workflow:

formula <- Loan_Status ~ Gender + Married + Dependents + Education +

Self_Employed + ApplicantIncome + CoapplicantIncome + LoanAmount +

Loan_Amount_Term + Credit_History + Property_Area

recipe_spec <- recipe(formula, data = train_data) |>

step_dummy(all_nominal(), -all_outcomes())

model_spec <- logistic_reg(engine = "glm", mode = "classification")

tailor_spec <- tailor() |>

adjust_probability_threshold(threshold = tune())

wf <- workflow() |>

add_model(model_spec) |>

add_recipe(recipe_spec) |>

add_tailor(tailor_spec)Tune the workflow:

parameters <- extract_parameter_set_dials(wf) |>

update(threshold = threshold(range = c(0.1, 0.9)))

tune_result <- tune_bayes(wf, resamples = resamples,

metrics = cv_metrics,

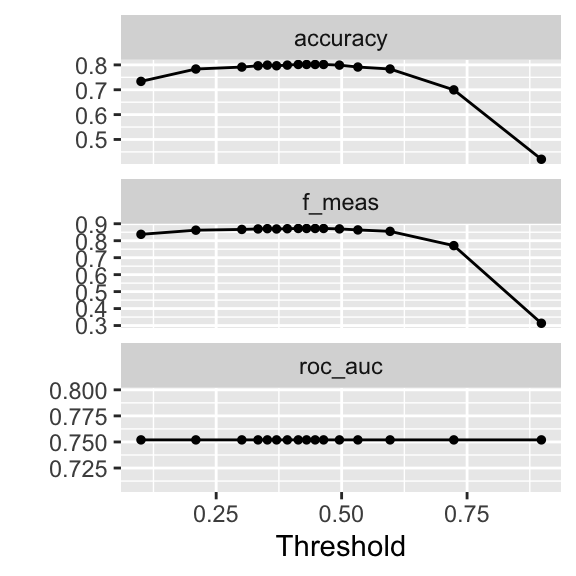

param_info = parameters, iter = 25)Figure 28.1 shows the tuning results. We can see that the F-measure is maximized at a threshold of around 0.38. Accuracy is practically unchanged for thresholds between 0.38 and 0.7. ROC-AUC is threshold independent and therefore unchanged.

autoplot(tune_result)

The “optimal” threshold is:

best_threshold <- tune_result |>

select_best(metric = "f_meas")

best_threshold# A tibble: 1 × 2

threshold .config

<dbl> <chr>

1 0.464 iter01 We finalize the model and train it using the full training set:

final_wf <- finalize_workflow(wf, best_threshold)

result_cv <- fit_resamples(final_wf, resamples, metrics = cv_metrics,

control = cv_control)

fitted_model <- final_wf |> fit(train_data)Estimate model performance using the cross-validation results and the holdout data:

cv_results <- collect_metrics(result_cv) |>

select(.metric, mean) |>

rename(.estimate = mean) |>

mutate(result = "Cross-validation", threshold = best_threshold$threshold)

holdout_predictions <- augment(fitted_model, new_data = holdout_data)

holdout_results <- bind_rows(

c(roc_auc(holdout_predictions, Loan_Status, .pred_Yes,

event_level = "first")),

c(f_meas(holdout_predictions, Loan_Status, .pred_class)),

c(accuracy(holdout_predictions, Loan_Status, .pred_class))) |>

select(-.estimator) |>

mutate(result = "Holdout", threshold = best_threshold$threshold)The performance metrics are summarized in the following table.

bind_rows(

cv_results,

holdout_results,

) |>

pivot_wider(names_from = .metric, values_from = .estimate) |>

kableExtra::kbl(digits = 3) |>

kableExtra::kable_styling(full_width = FALSE)| result | threshold | accuracy | f_meas | roc_auc |

|---|---|---|---|---|

| Cross-validation | 0.464 | 0.802 | 0.872 | 0.752 |

| Holdout | 0.464 | 0.835 | 0.893 | 0.733 |

We can see that the reduced threshold leads to a higher accuracy.

Code

The code of this chapter is summarized here.

Show the code

knitr::opts_chunk$set(echo = TRUE, cache = TRUE, autodep = TRUE,

fig.align = "center")

library(tidyverse)

library(tidymodels)

filename <- paste0(

"https://gedeck.github.io/machine-learning-with-tidymodels/",

"datasets/loan_prediction.csv"

)

data <- read_csv(filename, show_col_types = FALSE) |>

drop_na() |>

mutate(

Gender = as.factor(Gender),

Married = as.factor(Married),

Dependents = gsub("\\+", "", Dependents) |> as.numeric(),

Education = as.factor(Education),

Self_Employed = as.factor(Self_Employed),

Credit_History = as.factor(Credit_History),

Property_Area = as.factor(Property_Area),

Loan_Status = factor(Loan_Status, levels = c("Y", "N"),

labels = c("Yes", "No"))

) |>

select(-Loan_ID)

set.seed(123)

data_split <- initial_split(data, prop = 0.8, strata = Loan_Status)

train_data <- training(data_split)

holdout_data <- testing(data_split)

resamples <- vfold_cv(train_data, v = 10, strata = Loan_Status)

cv_metrics <- metric_set(f_meas, roc_auc, accuracy)

cv_control <- control_resamples(save_pred = TRUE)

formula <- Loan_Status ~ Gender + Married + Dependents + Education +

Self_Employed + ApplicantIncome + CoapplicantIncome + LoanAmount +

Loan_Amount_Term + Credit_History + Property_Area

recipe_spec <- recipe(formula, data = train_data) |>

step_dummy(all_nominal(), -all_outcomes())

model_spec <- logistic_reg(engine = "glm", mode = "classification")

tailor_spec <- tailor() |>

adjust_probability_threshold(threshold = tune())

wf <- workflow() |>

add_model(model_spec) |>

add_recipe(recipe_spec) |>

add_tailor(tailor_spec)

parameters <- extract_parameter_set_dials(wf) |>

update(threshold = threshold(range = c(0.1, 0.9)))

tune_result <- tune_bayes(wf, resamples = resamples,

metrics = cv_metrics,

param_info = parameters, iter = 25)

autoplot(tune_result)

best_threshold <- tune_result |>

select_best(metric = "f_meas")

best_threshold

final_wf <- finalize_workflow(wf, best_threshold)

result_cv <- fit_resamples(final_wf, resamples, metrics = cv_metrics,

control = cv_control)

fitted_model <- final_wf |> fit(train_data)

cv_results <- collect_metrics(result_cv) |>

select(.metric, mean) |>

rename(.estimate = mean) |>

mutate(result = "Cross-validation", threshold = best_threshold$threshold)

holdout_predictions <- augment(fitted_model, new_data = holdout_data)

holdout_results <- bind_rows(

c(roc_auc(holdout_predictions, Loan_Status, .pred_Yes,

event_level = "first")),

c(f_meas(holdout_predictions, Loan_Status, .pred_class)),

c(accuracy(holdout_predictions, Loan_Status, .pred_class))) |>

select(-.estimator) |>

mutate(result = "Holdout", threshold = best_threshold$threshold)

bind_rows(

cv_results,

holdout_results,

) |>

pivot_wider(names_from = .metric, values_from = .estimate) |>

kableExtra::kbl(digits = 3) |>

kableExtra::kable_styling(full_width = FALSE)